Big Blew It! IBM Crashes Most Since ’60s Amid CapEx Woes; Goldman Warns Over ‘Software Bear Case’

Big Blew It! IBM Crashes Most Since ’60s Amid CapEx Woes; Goldman Warns Over ‘Software Bear Case’

Summary:

- Wall Street Desks Stunned

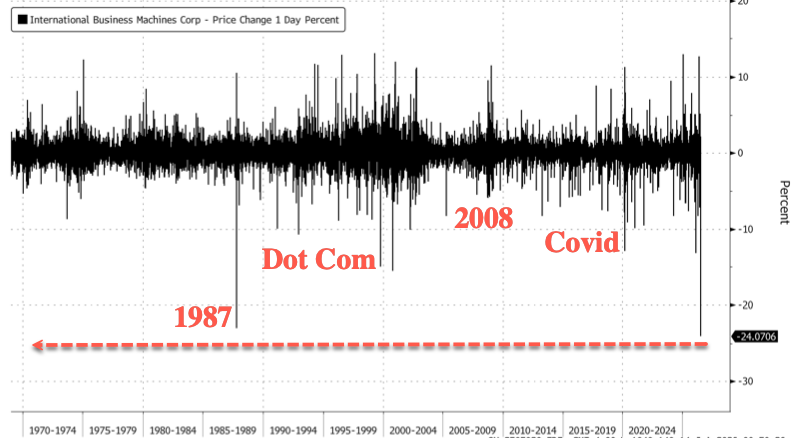

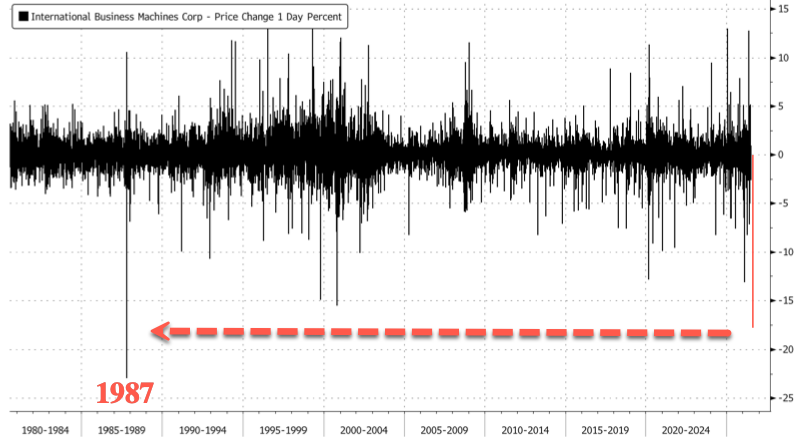

- IBM Shares Crash Most On Record, Exceeding Dot Com & 1987 Crashes

- CEO Arvind Krishna Blamed Preliminary 2Q Results on “Shifting” Customer CapEx Spending

IBM’s surprise second-quarter warning blindsided traders Tuesday morning, raising new concerns that enterprise technology budgets are being redirected toward AI infrastructure at the expense of traditional software and IT services.

Shares plunged 24% in the first 20 minutes of New York trading. Should those losses hold through the close, IBM would suffer its largest one-day crash on record, based on Bloomberg trading data going back to 1968.

Here’s what Wall Street’s top desks are saying in first takes:

UBS analyst Robert Ruple:

The big news this morning was a surprising negative preannouncement by IBM, down 22%, with Q2 sales of $17.2 bn versus $17.8 bn expected and EPS of $2.93 versus $3.02. Citing unanticipated capex reprioritization impacting client buying patterns with numerous large deals failing to close on time, cybersecurity distractions and some supply chain-related impact where they saw clients shift their quarterly capex spend toward servers, storage, and memory purchases to secure supply-constrained infrastructure (thanks to AI boom) ahead of expected price increases. This redirection of budgets towards AI has been a topic that Karl Keirstead/team have been articulating as potential risk for some time (particularly for incumbent SaaS suppliers and IT Services companies), which sounds like a harbinger of commentary that could be further accentuated by other software, IT services and hardware-related companies as Q2 reporting season progresses that is sure to weigh on sentiment incrementally.

David Vogt provides his initial thoughts on the IBM miss and these results suggest that enterprise IT spending pressures are hitting sooner than investors anticipated, leading to a revenue shortfall and non-GAAP EPS guidance of $2.93, below both expectations and consensus. The primary driver was weakness in IBM’s zSeries mainframe cycle, which hurt its high-margin Transaction Processing (TP) business. While Red Hat delivered solid 11% constant-currency growth and recently acquired assets such as HashiCorp and Confluent performed well, these positives were overshadowed by a sharp decline in TP revenue, which appears to have fallen in the mid-teens year over year and represents nearly 30% of IBM’s Software segment. As a result, investors are likely to reassess IBM’s long-term software growth outlook, particularly for 2027 and beyond, as rising infrastructure costs and tightening IT budgets weigh on demand. These results reinforce concerns that stronger growth areas like Red Hat may not be sufficient to offset prolonged weakness in TP business, increasing pressure on IBM to pursue larger acquisitions or other growth initiatives to sustain its software growth trajectory remaining at neutral.

Goldman analysts:

IBM: Negatively preannounced Q2 results this morning, with Revenues coming in well below estimates on shortfall led by Software & Infrastructure performance. Stock -17% in pre. Prelim Q2 Revenue missed estimates ($17.2bn vs. cons $17.9bn). Company said “did not anticipate magnitude of CapEx reprioritization.” Shortfall vs. consensus was led by “Software and Infrastructure performance shortfall.” Mgmt commentary: “What played out was worse than our expectations, driven by a shortfall in our Z performance and the associated software stack, primarily in Transaction Processing. In the last few weeks of June, we saw clients shift their quarterly capex spend toward servers, storage, and memory purchases to secure supply-constrained infrastructure ahead of expected price increases. This dynamic impacted client buying patterns. While we anticipated some supply chain related impact in our expectations, we did not anticipate the magnitude of the capex reprioritization.” BOTTOM LINE: This should fully play into the Software bear case, and would imagine should drive fairly broad-based weakness across software + services layer today (most names down 3%+ early in pre).

Goldman analyst James Schneider:

What happened: We expect the stock to trade meaningfully lower following IBM’s negative pre-announcement this morning, which was driven by a shortfall in Infrastructure and Software to a lesser extent. We believe the mainframe shortfall reflects client demand re-prioritization toward near-term server and other hardware purchases given surging memory and component prices, a dynamic consistent with what peers such as Dell and HP have cited. This reprioritization also drove a shortfall in Transaction Processing because of perpetual licenses tied to new mainframe purchases. In addition, we believe the company’s Data & Automation software segment saw weaker demand due to company-specific execution issues. Red Hat results were in line with expectations at a growth of 11% in the quarter. We leave our estimates unchanged for now, pending further color from the company on next week’s earnings call on updated 2026 guidance and potential remediation efforts.

BNP Paribas analyst Stefan Slowinski:

IBM is trading -22% pre-market on a disappointing Q2 earnings pre-announcement, driven by the company’s Infrastructure (hardware) and Software businesses, blamed on capex reprioritization (i.e. crowding out) and delays caused by cybersecurity uncertainty, with no indication of any improvements yet.

Barclays analyst Andrew Keches:

The news: IBM pre-released selected 2Q26 results alongside a letter to shareholders, with revenue below expectations amid shortfalls in Software and Infrastructure. Revenue came in at $17.2bn overall (vs. $17.9bn est.), while at the segment level, Software grew 5% y/y (vs. +11% est.), Infrastructure fell 7% (vs. -3% y/y est.), and Consulting was flat (vs. +2% y/y est.). The company attributed most of the underperformance to unexpected shifts in clients’ late-quarter budget allocations toward securing supply-constrained infrastructure ahead of price increases. IBM also acknowledged an execution component, with numerous large deals failing to close on schedule.

The context: Today’s update comes at a sensitive point for IBM’s investment narrative. Software has become the company’s primary growth engine, and management had increasingly framed AI as additive to the software stack rather than a source of disruption. Today’s update complicates that framing as the shortfall was concentrated in Z and the associated Transaction Processing software stack, with clients redirecting spending toward supply-constrained servers, storage, and memory. The key debate, in our view, will be whether this represents a temporary shift in the timing of enterprise purchases, or evidence that rapid AI infrastructure investment is beginning to crowd out portions of traditional software spending.

Our take: Clearly the results are a disappointment and the equity move alone (-20% premkt as of writing) will be a drag on credit performance. Credit metrics would not be impacted in a meaningful way, but the development adds to already weak sentiment in the name. We are mindful of the pointed M&A comments made on the last call (valuations attractive, appetite could be higher than in normal years), and although this pre-release suggests nothing about the topic, weak results will add to the overhang. Moreover, IBM spreads have held in better than most A/BBB TMT curves in the recent TMT sell off, widening the differential to BBB telco and single-A software curves such as NOW. To be clear, we view this quarter as a one-off rather than a step function in mainframe and software demand and also acknowledge that IBM has the cash flow to absorb medium sized M&A, but the impetus to step in and defend the structure at these levels is not obvious to us.

Laterals: The clearest potential beneficiaries from IBM’s commentary are hardware providers levered to the spending categories being prioritized, such as servers and storage at DELL and HPE, and memory at MU. Conversely, the update may reinforce concerns around software names broadly, as well as consulting and IT-services businesses such as ACN and KD, if AI infrastructure investment is crowding out other portions of enterprise technology budgets. That said, we are somewhat surprised by the breadth of the read-through across the group so far this morning. IBM explicitly acknowledged company-specific execution issues, including large deals that failed to close on schedule, and the decision to pre-release more than a week before its scheduled earnings call suggests that its shortfall may be more outlier than industry-wide. We understand that this is a “sell first, ask questions later” market, but we would be cautious about treating IBM’s results as a 1:1 read-through to every software and services company.

Laterals: The clearest potential beneficiaries from IBM’s commentary are hardware providers levered to the spending categories being prioritized, such as servers and storage at DELL and HPE, and memory at MU. Conversely, the update may reinforce concerns around software names broadly, as well as consulting and IT-services businesses such as ACN and KD, if AI infrastructure investment is crowding out other portions of enterprise technology budgets. That said, we are somewhat surprised by the breadth of the read-through across the group so far this morning. IBM explicitly acknowledged company-specific execution issues, including large deals that failed to close on schedule, and the decision to pre-release more than a week before its scheduled earnings call suggests that its shortfall may be more outlier than industry-wide. We understand that this is a “sell first, ask questions later” market, but we would be cautious about treating IBM’s results as a 1:1 read-through to every software and services company.

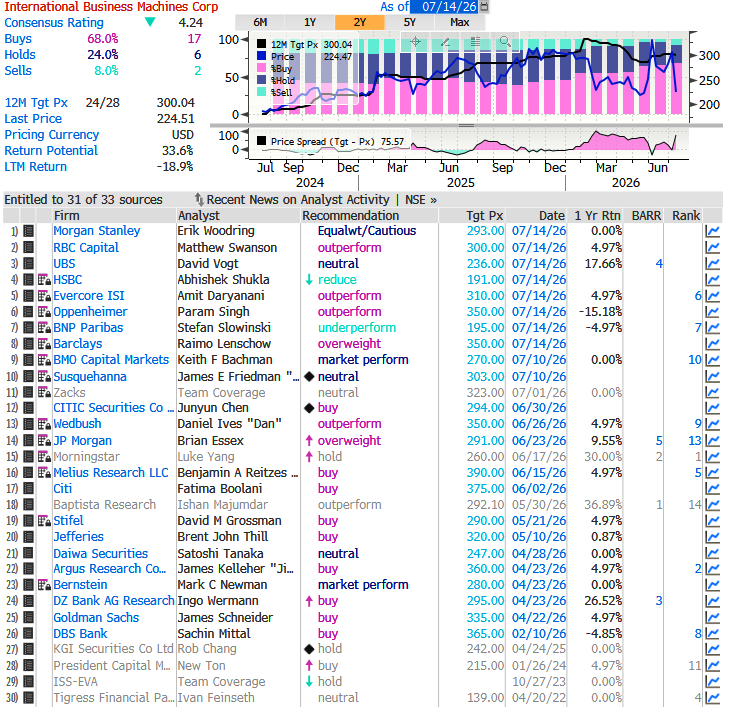

Bloomberg tracked analysts have an average 12-month price target of $300 on IBM, highlighting how far Wall Street expectations had run ahead of the shock preliminary second-quarter results earlier. Of the 25 analysts covering the stock, 17 rate it a Buy, six are Neutral and just two recommend selling.

SaaSpocalypse Is Back: IBM Crashes Most Since 1987 As Customers Abruptly “Shift CapEx Spending”

IBM shares plunged almost 20% in premarket trading, putting the stock on track for its worst intra-day collapse since the infamous Oct. 19, 1987.

Worse than the Dot Com crash…

The catalyst for the selloff was IBM CEO Arvind Krishna’s letter to investors outlining preliminary second-quarter results.

Here is what’s key:

- IBM CEO: DID NOT ANTICIPATE MAGNITUDE OF CAPEX REPRIORITIZATION

Traders were likely caught off guard by a 7% decline in infrastructure revenue, raising new concerns about demand across one of IBM’s key business segments.

Here are the preliminary 2Q results:

-

Revenue of $17.2 billion, up 1%

-

Software revenue up 5%

-

Consulting revenue flat, up 1% at constant currency

-

Infrastructure revenue down 7%

Krishna detailed in the letter to investors that customers unexpectedly redirected their June technology budgets toward servers, storage and memory to secure scarce equipment before anticipated price increases.

In return, that left less money and management attention available for IBM’s z17 mainframes and related transaction-processing software. Deals IBM expected to close during the quarter were delayed or pushed into later periods, rather than necessarily canceled outright.

Here are Bloomberg headlines:

-

IBM CEO: SAW CLIENTS SHIFT QUARTERLY CAPEX SPEND IN JUNE

-

IBM CEO: THIS DYNAMIC IMPACTED CLIENT BUYING PATTERNS

Signaling a return to the SaaSpocalypse (client spend shifting from commoditized software to constrained hardware), Krishna wrote:

When we discussed our expectations with you in April, we noted that we would be wrapping on the launch of z17 in the second quarter.

Given this was the strongest start to a mainframe program in our history, we expected Infrastructure revenue to decline low-single digits for the year, beginning this quarter.

What played out was worse than our expectations, driven by a shortfall in our Z performance and the associated software stack, primarily in Transaction Processing.

In the last few weeks of June, we saw clients shift their quarterly capex spend toward servers, storage, and memory purchases to secure supply-constrained infrastructure ahead of expected price increases.

This dynamic impacted client buying patterns. While we anticipated some supply chain related impact in our expectations, we did not anticipate the magnitude of the capex reprioritization.

In addition, clients were distracted with rapidly-evolving, industry-wide cybersecurity concerns in the quarter.

Krishna also admitted: “We did not adapt and move quickly enough,” with large deals failing to close on expected timelines.

The key question is whether IBM is emerging as an early warning sign that the AI boom is beginning to crack, with a potential “token revolt” taking shape as customers push back against surging AI costs.

Tyler Durden

Tue, 07/14/2026 – 10:36